How Does Bitcoin Work? A Detailed Guide for Beginners

Origins of Bitcoin: The White Paper

Bitcoin, the first-ever cryptocurrency, was introduced to the world via a white paper titled "Bitcoin: A Peer-to-Peer Electronic Cash System".

The mysterious and pseudonymous individual or group of people known as Satoshi Nakamoto (2008) authored this paper.

His vision was to create a electronic cash system that was "completely decentralized, with no central server or trusted parties, because everything is based on crypto proof instead of trust".

While there was little fanfare at the time, Bitcoin would soon lay the groundwork for a financial revolution.

Satoshi Nakamoto: The Enigmatic Creator

An exploration of Bitcoin's origins would be incomplete without firstly discussing its mysterious creator, Satoshi Nakamoto.

However, the reality is that Nakamoto's identity remains unknown. His name is pseudonymous, and despite numerous theories and claimed 'unmaskings', his identity or identities have never been definitively confirmed.

This anonymity has fueled speculation and mystery around Bitcoin's origins. However, it's Nakamoto's groundbreaking work and philosophy that have had a lasting impact.

Satoshi Nakamoto valued ideas that were revolutionary for their time.

He believed in a financial system where no single person or institution holds the power, rather everyone who uses Bitcoin shares in its control.

He was a strong advocate for freedom in transactions, where once a payment is made, it can't be reversed. This helps prevents fraud by eliminating the possibility of chargebacks, often exploited in traditional financial systems. In addition, it instills a sense of personal responsibility and trust in the system.

Privacy was also important to Nakamoto, as Bitcoin offers a way for people to protect their identity in financial dealings.

He also designed Bitcoin to be steady in its value, similar to how gold is limited in the world.

Finallt, he wanted Bitcoin's technology to be open to everyone, encouraging transparency and inviting improvements.

What we know about Nakamoto’s thoughts originate in discussions about Bitcoin on online forums, most notably on the BitcoinTalk forum.

BitcoinTalk.org was created in 2009 by Nakamoto as a place for people to talk about Bitcoin and share ideas and developments.

He also communicated via email, particularly with people involved in the early development and adoption of Bitcoin. Some of these email exchanges have been made public, providing additional insight into his views and the technical aspects of Bitcoin.

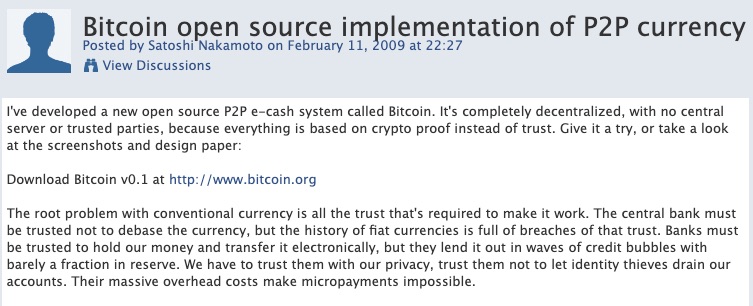

Satoshi Nakamoto's post titled "Bitcoin open source implementation of P2P currency" on the P2P Foundation website, February 11, 2009. Considered one of the earliest public announcements regarding Bitcoin. Source

Satoshi Nakamoto's post titled "Bitcoin open source implementation of P2P currency" on the P2P Foundation website, February 11, 2009. Considered one of the earliest public announcements regarding Bitcoin. Source

In 2010, Nakamoto stopped participating in these forums and ceased all public communication. His last known correspondence to the Bitcoin community was sent on April 23, 2011, to Bitcoin developer Mike Hearn, in which he stated that he had "moved on to other things" and that Bitcoin was "in good hands with Gavin [Andresen] and everyone."

At the time of Nakamoto’s disappearance, he reportedly had an estimated 1.1 million Bitcoin in his possession. This immense fortune, if accessed, would place him among the wealthiest individuals in the world, and yet, intriguingly, these Bitcoin have remained untouched to this day.

Nakamoto’s influence has been substantial, and his beliefs continue to guide Bitcoin’s development, as well as the development of other cryptocurrencies.

Bitcoin and the double-spend problem

Values aside, one of Bitcoin’s most compelling offerings is how it addresses the double-spend problem in digital currencies. In order to understand the double-spending problem, let's start by compare physical money with digital money.

Physical Money vs. Digital Money

From the dawn of human civilization to our digital era, trade has always been at the center of our existence, evolving to facilitate human interactions and socio-economic growth.

In the beginning, there was no money.

Early humans survived by simply bartering goods and services. This practice, though primitive, laid the groundwork for a system that would form the basis of modern economies. It was a system built on trust, reciprocity and the mutual exchange of value.

However, this barter system had its limitations: a lack of a common measure of value and difficulty in storing value.

In response, humans created a medium of exchange - money. The first iteration of money took the form of commodities: physical objects that had intrinsic value such as gold, silver, salt, and cattle. They were tangible, scarce, and widely accepted, making them suitable for serving as a store of value, unit of account, and medium of exchange.

Back in the day, this worked.. really well.

Let's imagine for a moment that you and I both inhabit prehistoric versions of ourselves. We find ourselves, under a blazing sun, in an bustling ancient market square,

You have offered to trade me your finely crafted stone axe for one of my prized goats.

And just like that, without a word spoken, our transaction is complete. You're now the proud owner of a goat, and I a new axe!

This exchange didn't occur in a void. I was there, you were there, and so was the goat.

Bahh.

Bahh.

No witnesses were needed for this exchange. Elder Galdor, the wise and respected leader of our village, had no role to play in this simple transaction. He didn't have to affirm that yes, indeed, the goat and the axe had changed owners.

The goat, once traded, is now completely yours. It doesn't attempt to return, it doesn't even look back at me. Grateful, much..! 🙄

As the new owner, you now decide its fate. You can choose to trade it with your friend for something else. Your friend may pass it on further still.

Now, isn't this what trade has always been about?

Whether it's trading goats, a sheaf of grain, a piece of finely crafted pottery, a gold nugget, or a silver coin, the essence remains the same.

As societies evolved, so did the things we traded. Precious metal coins were introduced by ancient cultures. The Chinese then began using paper money as early as the 9th century during the Tang Dynasty. Throughout the Middle Ages and Renaissance, banking practices matured, and paper money became widely accepted.

With physical money, double-spending is inherently impossible. If you have a dollar bill and you use it to buy a coffee, you physically relinquish that bill to the barista. You no longer have the dollar, so you can't spend it again.

With the advent of the internet, people began to envision new kinds of currencies that were purely digital and outside of government jurisdiction.

Early embodiments of these digital currencies included DigiCash and E-Gold.

However, with digital currencies, things are far from as straightforward as exchanging goats for cutting-edge stone tools.

That's because, like everything that's digital, digital currencies are essentially digital files.

If you've ever copied a file on your computer or shared a photo online, you know that it's quite easy to make perfect duplicates of digital information. So, what's stopping someone from duplicating their digital money and spending it multiple times?

This is the double-spend problem.

The Bitcoin ledger

Early digital currencies tried to prevent double-spending by using a central system to check and track transactions. While this did help control double-spending, it also created new problems that proved little different from digital transactions of fiat money.

For example, when you make a bank transfer or use an online platform like PayPal to send $100 to your buddy in Alaska, it's not like an actual $100 bill gets physically flown over there and handed to them directly.

What's really happening is a simple database update, happening within central servers, and not over skies!

This database, in a financial context, is referred to as a ledger.

The term "ledger" is borrowed from traditional accounting, where a ledger was a book or other collection of records in which a company's or individual's financial transactions were documented.

We trust institutions to constantly update their ledgers to reflect the latest state of each account involved in the transaction. They can add $10 to Jane Doe's account, subtract $10 from yours, or make any other adjustments they deem necessary

But relying on a trusted party comes with some inherent complications.

The reality is, you don't hold the reins. You have effectively handed the banks control of your finances.

Moreover, their power extends beyond maintaining an up-to-date ledger.

They can alter their terms of service without your consent, block or delay your payments, freeze your account, or even adjust your balances according to their discretion.

But hold on.. Financial institutions have to adhere to certain legal obligations!

Yes.. until the government says otherwise.

A stark example of this was observed during the financial crisis in Greece, where banks imposed strict capital controls, significantly limiting access to one's own money.

You could opt to hoard hard cash, but navigating today's digitalized world with physical currency is ever an increasing challenge. Not only are more transactions than ever being conducted electronically but the convenience and ubiquity of digital payment options have also transformed our expectations of commerce.

Whether it's shopping online, ordering a food delivery, or subscribing to a streaming service, digital payments have become the norm, rendering cash less practical.

What we need is the digital equivalent of our ancient market square..

Enter.. The Blockchain!

Bitcoin took the concept of a ledger but removed the need for institutions.

It does this through its distributed ledger and blockchain technology.

A distributed ledger is a type of database that's spread all over the world.

This Bitcoin ledger maintains a complete record of all past and present transactions, including the ownership of each Bitcoin in circulation.

All transactions are periodically packaged into a block. The block contains details about the transactions, along with two important pieces of information: a unique code called a "hash" and the hash of the previous block.

The hash is generated from the information within the block itself, which makes it unique to that block - such as, the various sender and receiver addresses, as well as the exact times of the various transactions enclosed. Any change in the block's information, including transaction details or the order of transactions, would result in a different hash. This mechanism helps to maintain the integrity and security of the data in the ledger.

The hash is used as a kind of 'fingerprint' that ensures the integrity of the data, as any change to the data would result in a completely different hash. (source: Wikipedia)

The hash is used as a kind of 'fingerprint' that ensures the integrity of the data, as any change to the data would result in a completely different hash. (source: Wikipedia)

Each hash also contains the hash of the most recent block. This essentially create a link to the block that came before it. This eventually forms a chain of blocks, which is why the technology is called blockchain. When a new block is ready, it is added to the end of this chain.

Linking hashes ensures that the blocks remain connected. If the information in a block were to be changed, its hash would change. This would break the link with the next block.

This setup makes it extremely hard for anyone to change information once it has been added to the blockchain.

If someone were to tamper with the data in a block, it would change that block's hash. But because that altered hash is also part of the next block's hash, the tampering would cause a domino effect, invalidating the hashes of all subsequent blocks in the chain.

This makes it immediately obvious if someone attempts to change information in the blockchain.

Everyone participating in the blockchain network can view all the blocks, from the first to the most recent. This transparency is a key feature of blockchain technology. However, the identities of those involved in transactions are protected through the use of special cryptographic keys.

But wait..! Who manages the blockchain?

Everyone!

Ok.. not everyone, but everyone who's operating a Bitcoin node.

A node is a computer connected to the Bitcoin network. In order to become a node, you have to first download and install the Bitcoin Core client software. Through that software, you can connect to the ledger and even download a copy of the entire ledger - over 500 GB as of August 2023.

There are three kinds of nodes on the Bitcoin network:

| Full nodes | Mining nodes | Light nodes |

|---|---|---|

| These nodes download the entire blockchain and enforce all the consensus rules of Bitcoin. They serve to validate transactions and blocks on the network, making the network more robust and decentralized. | These are full nodes that also perform mining. Just like a full node, a mining node will collect transactions and verify them. Mining nodes, however, go one step further than that. They add the block to the blockchain. Running a mining node involves more computational power and energy consumption. | These are nodes that don't download the entire blockchain but rely on full nodes to provide them with the information they need. They are typically used to make transactions. |

There are now over 45,000 computers around the world that have downloaded and currently run a Bitcoin node.

Not only is the computing power of the network spread around the world on thousands of different computers, together they keep it running.

Transactions are recorded and verified collectively. And, if the data is changed on one single node, it is quickly rejected by the wider network.

This is what blockchain technology is all about. A network of computers work in tandem to uphold the integrity of a network without the need for a central authority.

How does the Bitcoin blockchain work?

Every time Bitcoin is exchanged, a transaction is triggered that consists of an input (source of Bitcoin), amount, and output (destination wallet).

The transaction is then broadcasted to the distributed ledger and added to a queue of unconfirmed transactions on the network.

These transaction are bundled with others into a "block" every 10 minutes.

A block is similar to an Excel spreadsheet tab, equipped with 1000 rows. Once you've filled these 1000 rows, to continue documenting transactions, you need to open a new tab with an additional 1000 rows. This mirrors the function of new blocks in the blockchain system. The blocks can be compared to these fresh tabs in the Excel file.

One of the nodes picks it up from here and performs a basic level of transaction verification.

This includes

- Ensuring the sender has sufficient balance to make the transaction and hasn't attempted to double-spend their Bitcoin.

- Checking if the format of the transaction (the signature) is correct.

- Verifying that the input and output amounts match up, i.e., no Bitcoin is created or destroyed accidentally.

- Confirming that the sender is the actual owner of the Bitcoin being sent.

Once all the transactions in a block have been verified, it's time to permanently add that block to the blockchain.

That's where specifically mining nodes step in, which must solve a complex mathematical puzzle through a process called proof-of-work.

This puzzle involves finding a special number, known as a "nonce". They combine this nonce with the data from the block they're trying to add to the chain and then run it through a process called a "hash function".

The hash that results from a hash function is unique to each specific input of data. If you put the same data into the hash function, you'll get the same hash out every time. But if you make even a tiny change to the data and put it into the hash function, you'll get a completely different hash out.

There’s no such thing as being 1% towards solving a block. You don’t make progress towards solving it. After working on it for 24 hours, your chances of solving it are equal to what your chances were at the start or at any moment. It’s like trying to flip 37 coins at once and have them all come up heads. Each time you try, your chances of success are the same.

Now the goal of proof-of-work, is to produce an output that has the set number of leadings 0s.

For example, the hash for block #800,108, mined on 24 Jul 2023, is:

00000000000000000002a7c4c1e48d76c5a37902165a270156b7a8d72728a054

The block reward for that successful hash was 6.25 BTC and 0.1368 BTC in fees, 1,906 BTC were exchanged for a total transaction value (at the time) of $56,718,724.

But here's the tricky part: there's no way to know what nonce will result in a hash that meets the requirement without actually trying it. So, miners have to keep guessing different nonces and checking to see if the resulting hash meets the requirement. This involves a lot of trial and error and is a process that takes a lot of computational power.

When a miner finds the right nonce, they tell all the other miners, who check the work. If it's correct, the successful node gets the right to add the new block to the blockchain.

They are then rewarded with a certain amount of new Bitcoin (this is called the block reward), plus the transaction fees of the transactions included in the block.

Winning the chance to add a block to the Bitcoin blockchain is like winning a lottery. Each miner is constantly buying tickets (by doing computational work), and the more tickets you buy, the better your chances of winning. However, unlike a regular lottery, this one happens approximately every 10 minutes.

The "ticket" in this case is solving a complex mathematical problem. The more computational power a miner has, the faster they can guess the solution.

But there's a catch. If there are more miners (more overall computational power), the number of leading 0s increases making the problem harder to solve. This ensures that new blocks are still only added approximately every 10 minutes, no matter how many miners there are.

So, the chance of an individual miner winning this "lottery" and getting to add the next block depends on how much computational power they have compared to the total computational power of all the miners. The more power they have, the better their chances. But because there are so many miners in the Bitcoin network, the chance for any single miner to win is very low.

The current bitcoin block reward as of 2023 is 6.25 bitcoins. The reward for mining a new block is halved approximately every four years or precisely every 210,000 blocks.

This is a process called the “Halving”.

The halving events are a part of Bitcoin's monetary policy, encoded in its algorithm to control supply and reduce the rate of new coin creation over time. This halving process continues until the maximum supply of 21 million bitcoins is reached.

Bitcoin's supply is finite, capped at 21 million coins. As of August 2023, .... have been minded.

Referring to proof of work as mining is a bit of a misnomer, as it suggests the extraction of valuable resources similar to gold mining.

In the context of Bitcoin, the "valuable resources" are new Bitcoins, and the process involves computational work, not physical digging.

This is how new Bitcoin is minted. Mining is what is used to give Bitcoin its value.

Just like mining, it’s hard to mine gold or silver. Solving a really hard math problem is the digital equivalent and what gives Bitcoin it’s value.

Proof of work has led to the development of specialized hardware for Bitcoin mining, known as ASICs (Application-Specific Integrated Circuits), which are much more efficient at mining than general-purpose computers.

A mining farm of Genesis Mining located in Iceland. The picture shows mainly "Zeus scrypt" miners.

A mining farm of Genesis Mining located in Iceland. The picture shows mainly "Zeus scrypt" miners.

Bitcoin facts

- Bitcoin network is popular, so people are sending more than 7 transactions per second.